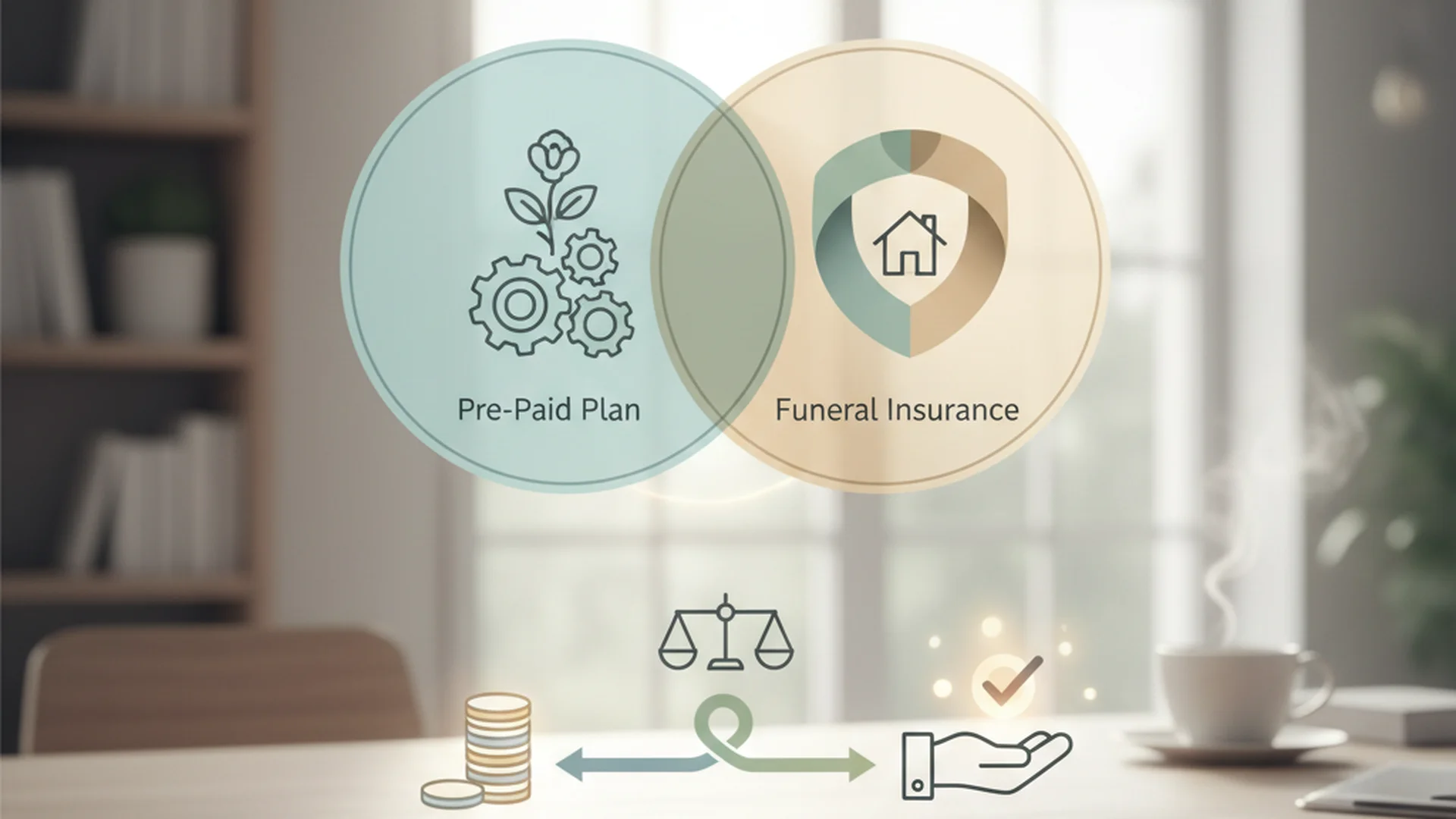

Key Takeaways

- Pre-paid plans lock in today’s prices but are often location-specific.

- Funeral insurance offers cash flexibility and portability but doesn't hedge against inflation.

- 2025 median funeral costs range from $10,500 to $15,000.

Deciding how to fund your final arrangements is one of the most responsible gifts you can leave for your family. However, navigating the choice between a pre-paid plan vs funeral insurance can feel overwhelming. As of 2025, the landscape of end-of-life planning is shifting rapidly, with rising costs and new digital options changing how we approach "the inevitable."

Whether you are looking for a way to lock in current service prices or you want to provide your beneficiaries with a flexible cash benefit, understanding the nuances of these two financial products is essential. In this guide, we will break down the costs, benefits, and risks of each to help you make an informed decision for your future.

Understanding Pre-Paid Funeral Plans

A pre-paid funeral plan is a contract you enter directly with a specific funeral home. You select the exact services you want—such as the type of casket, the viewing details, and the transportation—and pay for them either in a lump sum or through installments.

How Pre-Paid Plans Work

The primary appeal of a pre-paid plan is the "price lock." In most "guaranteed" contracts, the funeral home agrees to provide the services you’ve selected at today's prices, regardless of how much inflation rises by the time the services are needed.

Pros and Cons of Pre-Paid Plans

The main advantage is the peace of mind that comes from knowing every detail is handled. Your family won't have to guess what you would have wanted or navigate high-pressure sales during a time of grief.

However, the downside is rigidity. These plans are usually tied to a specific funeral home. If you move to another state or if the funeral home goes out of business, transferring the plan can be complicated and costly. You can find more detail on the specific mechanics of these plans in our Pre-Paid Funeral Plans Explained guide.

Understanding Funeral Insurance (Burial Insurance)

Funeral insurance, often called "Final Expense Insurance" or "Burial Insurance," is a life insurance policy specifically designed to cover end-of-life costs. Unlike a pre-paid plan, which is a contract for services, this is a financial product that pays out a tax-free cash benefit to your designated beneficiaries.

How Funeral Insurance Works

You pay a monthly premium to an insurance company. Upon your passing, the company issues a check to your beneficiary (usually a family member). That person can then use the funds to pay any funeral home they choose, or even use remaining funds to cover outstanding medical bills or legal fees.

Pros and Cons of Funeral Insurance

The greatest strength of insurance is its portability. It doesn't matter if you move from New York to Florida; the policy stays with you. It also offers the highest level of flexibility for your family.

The disadvantage is that it does not lock in funeral prices. If you buy a $10,000 policy today, but a funeral costs $20,000 in fifteen years due to inflation, your family will have to make up the $10,000 shortfall. For a deeper look at the financial implications, see our article on Are Pre-Paid Plans Worth It.

Side-by-Side Comparison: Burial Insurance vs Prepaid

Choosing between a prepaid plan or insurance depends on your priorities: price protection or flexibility.

| Feature | Pre-Paid Funeral Plan | Funeral Insurance (Final Expense) |

|---|---|---|

| Payee | The Funeral Home | Your Beneficiary (Family) |

| Price Protection | Locks in today’s service costs | No price lock; payout is fixed |

| Flexibility | Rigid; tied to specific services | High; cash can be used for anything |

| Portability | Difficult/Expensive to move | 100% portable across state lines |

| Payment Term | Usually paid in 3–10 years | Usually paid for life |

| Tax Status | Trust interest may be taxable | Death benefit is income tax-free |

Typical Costs and Inflation in 2025–2026

As of 2025, the Average Funeral Cost Breakdown shows that a traditional funeral with a vault and cemetery fees now ranges between $10,500 and $15,000.

The 6% Inflation Factor

Funeral costs have historically risen by about 6% annually. This makes the "price lock" of a pre-paid plan incredibly valuable over a long period. For example, a $12,000 funeral today could cost over $21,000 in just ten years. If you choose insurance, you must ensure your policy’s face value is high enough to account for this future growth.

Cremation vs. Burial Costs

The surge in cremation—projected to hit 63.4% this year—has introduced "direct cremation" as a budget-friendly alternative. These plans often cost between $900 and $2,500. Many people now opt for a pre-paid direct cremation plan combined with a smaller insurance policy to cover a celebration-of-life service later.

Real-World Scenarios: Which Should You Choose?

To better understand how these options play out, let’s look at three common real-world examples.

Example 1: The "Legacy Planner"

- Profile: Sarah, age 68, has lived in the same town for 40 years and plans to be buried next to her late husband in the local cemetery.

- Best Choice: Pre-Paid Funeral Plan.

- Why: Since Sarah is unlikely to move and knows exactly which funeral home she wants to use, a pre-paid plan allows her to lock in today’s prices and ensure her specific wishes are followed to the letter.

Example 2: The "Snowbird"

- Profile: Robert, age 65, spends half the year in Michigan and half the year in Arizona. He isn't sure where he will be when the time comes.

- Best Choice: Funeral Insurance.

- Why: Portability is Robert’s priority. An insurance policy ensures that his family has the cash available to handle arrangements regardless of which state he is in at the time of death.

Example 3: The "Digital Nomad Senior"

- Profile: Linda, age 62, wants a "green burial" and a simple digital memorial. She is tech-savvy and wants to minimize the "fuss" for her children.

- Best Choice: Hybrid Approach.

- Why: Linda might choose a pre-paid "eco-friendly" plan through a national provider and use a "Payable on Death" (POD) account to cover smaller expenses.

What matters: Choosing the right plan now prevents your family from making difficult financial decisions while they are grieving.

Trends Shaping the Industry in 2025 and 2026

The way we plan for the end of life is evolving. Here are four trends currently impacting the prepaid plan or insurance debate:

1. The Funeral Coverage Act (HSA Funds)

A major legislative push in 2025 aims to allow individuals to use tax-free Health Savings Account (HSA) funds to pay for funeral expenses. This could make HSAs a viable competitor to traditional funeral insurance for those who have accumulated significant health savings.

2. Digital-First Platforms

Over 36% of funeral firms now offer full online arrangement platforms. This allows you to browse prices and buy a pre-paid plan from your living room, much like any other e-commerce transaction.

3. Eco-Friendly and Carbon-Neutral Plans

Interest in "green funerals" has risen to over 61% in 2025. Many new pre-paid plans specifically offer biodegradable caskets and no-embalming options, often at a lower price point than traditional burials. If you are interested in these options, check out our guide on Biodegradable Urns.

4. Legacy AI

A 2026 trend involves "legacy AI," where pre-paid plans include the creation of AI-driven digital memorials. These platforms can host interactive guestbooks and digital "clones" that stay live for decades, providing a futuristic way to be remembered.

Common Mistakes to Avoid

When choosing between burial insurance vs prepaid, many consumers fall into the same traps. Avoid these four common errors:

- Ignoring "Cash Advance" Items: Many pre-paid plans only cover the funeral home’s internal services. They may exclude third-party costs like the obituary, flowers, clergy honorariums, or the cemetery plot itself. Always ask for a list of exclusions.

- The Communication Gap: Only 21% of people with a plan tell their family. If your family doesn't know you have a pre-paid plan with "Funeral Home A," they might accidentally pay for a second funeral at "Funeral Home B."

- Buying Too Young: Experts generally advise against pre-paid plans for those under 50. The risk of the funeral home closing or the person moving over a 30-year span often outweighs the benefit of the price lock. Insurance is usually a better vehicle for younger planners.

- Underestimating "Final" Expenses: A $5,000 policy might cover a simple cremation, but it won't cover unpaid medical bills, probate attorney fees, or the cost of a reception.

Frequently Asked Questions

What happens if the funeral home goes out of business?

Can I pay for my plan in installments?

Is the payout from funeral insurance taxable?

Is it possible to cancel a pre-paid plan?

What is a "Totten Trust" and is it better than insurance?

Conclusion

Choosing between a pre-paid plan vs funeral insurance ultimately comes down to your lifestyle and your desire for control. If you want to ensure your exact wishes are followed and you want to protect your family from future price hikes, a Pre-Paid Funeral Plan is likely your best bet.

If you value flexibility, portability, and the ability to provide your family with quick cash for any expense, funeral insurance is the superior choice. Regardless of which path you take, the most important step is to document your wishes and share them with your loved ones. For a step-by-step walkthrough, refer to our Complete Guide to Pre-Planning.

The main thing: By taking action today, you are removing a massive emotional and financial reality from your family's shoulders tomorrow.

Start Your Plan Today

Take the first step in securing your legacy and protecting your family's future.

Read the Pre-Planning Guide- 1.

- 2.

- 3.

- 4.

- 5.

- 6.

- 7.

Informational Purposes Only

This article is for informational purposes only and does not constitute legal, medical, or financial advice. Laws, costs, and requirements vary by location and individual circumstances. Always consult with qualified legal, medical, or financial professionals for advice specific to your situation.

Content reviewed by a licensed funeral director

Written by Julian Rivera

Licensed Funeral Director & Pre-Planning Specialist

Third-generation licensed funeral director (NFDA) with 15+ years in funeral service, specializing in pre-planning, cremation options, and consumer rights.